This move did not affect Taobao’s business in the slightest, and instead allowed it to colonise the entire consumer journey and become a platform that took users from the awareness phase through to loyalty. At the same time, the closed nature of its ecosystem made it the most important advertising channel for merchants on the platform. The custom management revenue of Alibaba, which includes commissions and advertising revenue, reached RMB 306.1 billion for the fiscal year 2021, which ended on March 31 – accounting for 43 per cent of total revenue.

More tech firms are starting to see the importance of offering a complete consumer journey on their platforms. Douyin, which plans to achieve 1 trillion RMB in GMV sales by 2021, took the plunge in October last year and started banning links from third-party e-commerce platforms (such as Tmall and JD.com) in livestreams, driving purchase intentions to its native Douyin store, and generating in-platform sales. The company launched its payment solution ‘Douyin Pay’ this January, facilitating the payment process for online shopping and purchasing virtual livestreaming gifts as well. At the same time, after suspending its pilot programme that offered redirection options to Tmall on selected KOL accounts, social commerce app RED launched launched the ‘one-account-one-store’ concept in August in a bid to develop its in-platform e-commerce business. By this point, the walled gardens created by China’s tech giants have started to take shape.

The Walls Are Coming down

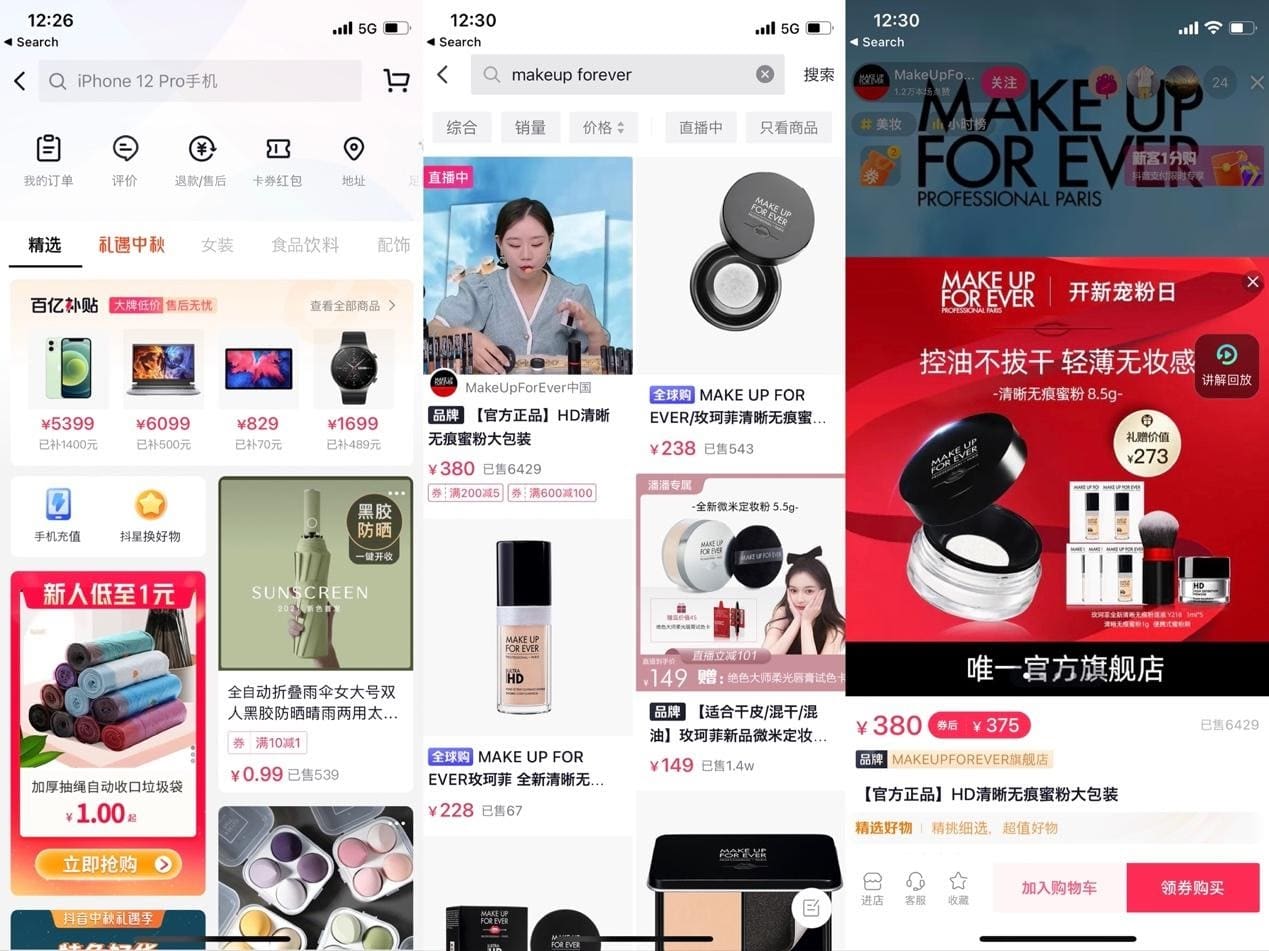

Early this year, Alibaba submitted Mini Program applications to WeChat for Taote (a discounted e-commerce platform to rival Pinduoduo) and Idlefish (a second-hand marketplace). This move will allow both platforms to support WeChat Pay and users to share links from Taote and Idlefish, on WeChat. This is the first time Alibaba and the WeChat ecosystem has displayed signs of integration since 2013.

Although integration with WeChat can reduce the traffic acquisition cost for Taobao/Tmall, given that Chinese consumers have already developed the habit of leveraging Taobao/Tmall as a search hub, this move will not impose a significant impact on Alibaba’s share of online retail today.

Alibaba’s share price saw a modest rise on the same day after the companies stated that they would open up their ecosystem on September 14, but e-commerce platforms invested in by Tencent, JD.com and Pinduoduo, dropped by 2.79 per cent and 1.4 per cent respectively.

Tencent holds a 15.6 per cent stake in Pinduoduo and a 16.9 per cent stake in JD.com through Huang River Investment Ltd. Both platforms have developed Mini Programs on WeChat, and their platform and products can be freely accessed within the WeChat ecosystem. It should be noted that Pinduoduo’s entire group-buying model is built on top of the immense traffic offered by WeChat, whose ecosystem facilitates the sharing of and participation in shopping activations among users. Given Taote’s strong ambitions of developing social commerce on WeChat – the e-commerce platform has a 78 per cent overlap with Pinduoduo in terms of users – the existing dominance of Pinduoduo in lower-tier markets might be shaken.

The liberalisation of ecosystems will also affect the e-commerce business on emerging platforms, such as short video platform Douyin. Its e-commerce business achieved a GMV of 500 billion RMB in 2020, but more than 300 billion worth of transactions happened outside its platform.

Although today’s current requirement of opening up external linking between platforms target only instant messaging applications like WeChat, other platforms such as Douyin will be at risk of losing traffic to third-party marketplaces. Jin Yechen, a media practitioner active in the Chinese digital sector, opined that Douyin and Kuaishou, which have been expanding their e-commerce presence, do not lack traffic. In fact, developing their supply chain will be the next focus. “Today, cooperating with more brands and distributors is the heart of the battle between these two short video platforms,” he adds.

After shutting down the external redirection option in livestreams, Douyin’s in-platform merchant supply chain has blossomed. From January 2020 to May 2021, merchants on the platform grew 32 times and the GMV generated on Douyin Store increased by 75 times. Users are now able to access the Douyin e-commerce page for exploring content and shopping via their homepage feeds, and it is rumoured that a standalone Douyin e-commerce app will be launched in October this year.